How to Manage Currency Exchange Risks: The 2026 Definitive Guide

In the contemporary global economy, the volatility of foreign exchange (FX) markets represents one of the most significant, yet frequently underestimated, variables in cross-border financial management. Whether overseeing a multi-million-dollar international event, managing a transcontinental supply chain, or coordinating a private acquisition in a secondary jurisdiction, the fluctuation of currency values can instantaneously erode profit margins and disrupt carefully calibrated budgets. The movement of a currency pair by a mere 5%—a common occurrence within a single fiscal quarter—can transform a viable project into a financial liability.

The challenge lies in the “temporal gap” between the commitment to a price and the actual settlement of the transaction. During this window, the relative value of the “functional currency” (the currency in which you report) and the “transactional currency” (the currency in which the vendor is paid) is subject to the macro-economic whims of central bank interest rate decisions, geopolitical instability, and speculative market sentiment. Consequently, a passive approach to currency—assuming that the spot rate at the time of invoice will be favorable—is not a strategy; it is a speculative gamble that carries substantial institutional and personal risk.

Mastering the mechanics of foreign exchange requires a departure from retail-level currency thinking toward a sophisticated understanding of “Financial Hedging” and “Operational Governance.” It demands a shift from viewing exchange rates as a fixed cost to treating them as a dynamic variable that must be actively managed through specific instruments and strategic maneuvers. This article serves as a technical deconstruction of the FX landscape, offering a definitive framework for stakeholders who recognize that fiscal discipline is incomplete without a rigorous plan for currency resilience.

Understanding “how to manage currency exchange risks”

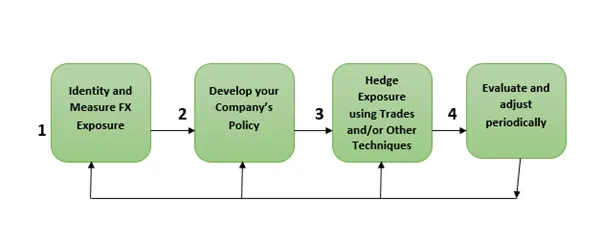

The phrase how to manage currency exchange risks defines the systematic process of identifying, quantifying, and mitigating the potential impact of adverse FX movements on a specific financial objective. From a multi-perspective view, this is not a one-size-fits-all endeavor. For a corporate treasurer, it involves “Balance Sheet Hedging” to protect shareholder value. For a wedding planner or private client coordinating a destination event, it involves “Cash Flow Hedging” to ensure that a $100,000 budget does not balloon into $115,000 due to an unexpected weakening of the dollar against the Euro or Baht.

A common oversimplification in this space is the belief that “hedging” is only for massive conglomerates. In reality, anyone engaging in a transaction where the payment date is more than 30 days in the future is exposed to “Transaction Risk.” There is also the “Economic Risk”—where a long-term shift in exchange rates impacts the competitiveness of a destination or a service provider over the years. Understanding these nuances is critical; an effective plan does not necessarily aim to “make money” on currency movements, but rather to “eliminate the unknown,” providing the stakeholder with “Budget Certainty.”

Oversimplification also risks ignoring the “Cost of Carry” and “Market Spreads.” Many individuals believe they are managing risk by simply holding physical foreign currency in a local bank account. However, this introduces “Opportunity Cost” (capital that could be earning interest elsewhere) and “Liquidity Risk” (the difficulty of moving that capital back if plans change). A professional management strategy utilizes specialized instruments—Forward Contracts, Limit Orders, and Options—to lock in rates without tying up massive amounts of liquid capital upfront. Ultimately, the goal is to stabilize the “Unit Cost” of the international endeavor.

The Systemic Evolution of the FX Market

To manage risk today, one must understand the historical context of currency volatility. Post-World War II, the Bretton Woods system established fixed exchange rates pegged to the U.S. Dollar. Volatility was virtually non-existent for the end-user. However, the collapse of this system in 1971 ushered in the era of “Floating Exchange Rates,” where the market—not the government—dictates value based on supply and demand.

The 2020s have introduced a new layer of complexity: “Algorithmic High-Frequency Trading.” Today, currency values can shift in milliseconds based on “Sentiment Data” scraped from news wires. This has increased “Intraday Volatility,” making the timing of a large currency transfer a critical point of failure. Furthermore, the rise of “Digital Currencies” and “Central Bank Digital Currencies” (CBDCs) is beginning to alter the plumbing of international settlements, potentially reducing “Transfer Friction” while introducing new “Regulatory Risks.”

Conceptual Frameworks: The Three Pillars of Exposure Analysis

Before deploying capital, a manager must categorize their exposure using these three diagnostic models.

1. The “Transaction Exposure” Matrix

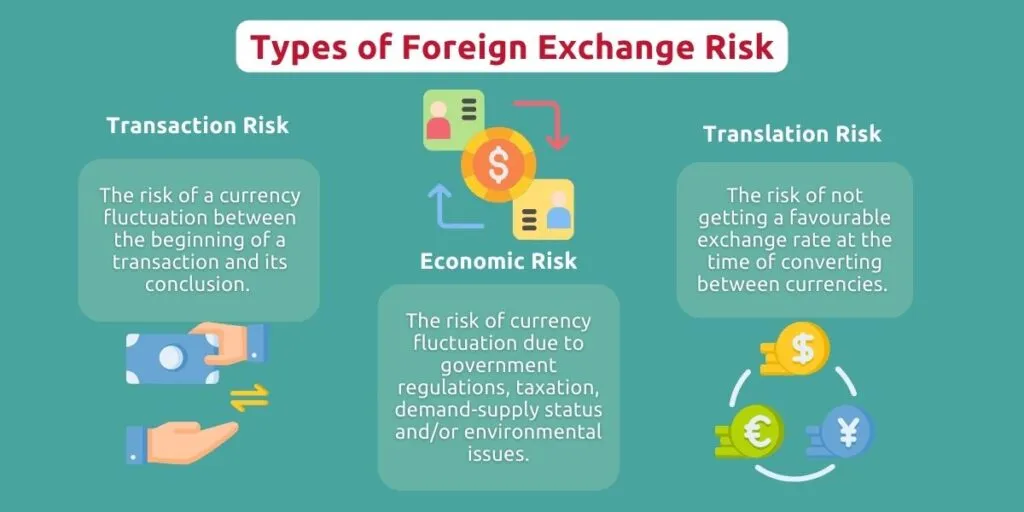

This model measures the risk of a specific, legally binding contract. If you sign a venue contract for €50,000 today for a wedding in 2027, your Transaction Exposure is the difference between today’s rate and the rate on the day of final payment. This is the most common risk and the easiest to hedge using a “Forward Contract.”

2. The “Translation Exposure” Framework

Primarily relevant for organizations with international assets, this framework looks at how the value of those assets fluctuates on the balance sheet when converted back to the home currency. While it doesn’t always impact immediate cash flow, it can affect “Credit Capacity” and “Borrowing Power.”

3. The “Economic (Operating) Exposure” Model

This is a “Macro” view. It assesses how a sustained change in currency value affects the long-term viability of a project. For example, if the Japanese Yen stays perpetually weak, a destination wedding in Tokyo becomes more attractive over a three-year planning horizon, potentially drawing more guests but increasing the cost of imported goods (like European wines or specialty florals) used at the event.

Key Categories of FX Hedging and Strategic Trade-offs

Choosing the right instrument is the first strategic hurdle in managing currency exchange risks.

| Instrument | Mechanism | Primary Advantage | Main Constraint |

| Spot Contract | Buying currency at the current live market rate. | Instant liquidity; simple. | Zero protection against future volatility. |

| Forward Contract | Locking in a rate today for a date in the future. | Total “Budget Certainty”; no upfront cost. | Mandatory execution; no benefit if the rate improves. |

| Limit Order | Automatically buying when a currency hits a specific “Target Rate.” | Captures favorable market “Spikes.” | The target rate may never be hit; no protection if the rate drops. |

| FX Option | Paying a “Premium” for the right (but not obligation) to buy at a rate. | Protection against downside; keeps upside potential. | Non-refundable “Premium” cost (like insurance). |

| Currency Swapping | Exchanging principal and interest in two different currencies. | Ideal for long-term projects (12+ months). | High administrative and legal complexity. |

| Natural Hedging | Matching local income with local expenses. | Eliminates the need for conversion. | Only possible if you have revenue in the foreign currency. |

Decision Logic: The “Certainty vs. Opportunity” Pivot

If the budget is rigid and cannot tolerate even a 2% increase, the Forward Contract is the superior choice. If the stakeholder has a more flexible “Risk Appetite” and wants to benefit if the home currency strengthens, an FX Option provides a safety net while allowing for “Participation” in favorable market movements.

Detailed Real-World Scenarios: Managing the Temporal Gap

Scenario A: The “Sudden Central Bank” Shift

-

Context: A U.S.-based corporation planning a leadership summit in London with a £500,000 budget.

-

The Conflict: The Bank of England unexpectedly raises interest rates by 0.5%, causing the Pound to surge against the Dollar.

-

The Failure: The corporation relied on “Spot” purchases. Within 24 hours, the cost of the event in USD terms rises by $35,000.

-

The Solution: A “Layered Hedging” strategy where 50% of the Pounds were secured via a Forward Contract six months prior, and the remaining 50% were managed via “Limit Orders.”

Scenario B: The “Currency Peg” Collapse

-

Context: A wedding in a country that “Pegs” its currency to the USD (e.g., in the Caribbean or parts of the Middle East).

-

The Conflict: Due to economic pressure, the local government “De-pegs” or devalues the currency.

-

The Second-Order Effect: While the USD now buys more local currency, local vendors immediately raise their prices to compensate for inflation.

-

The Strategy: Contracts should be denominated in USD whenever possible in “Pegged” economies to shift the “Devaluation Risk” to the vendor, who is more equipped to handle local inflation.

Economic Dynamics: Direct Costs vs. The Reliability Premium

A professional audit of how to manage currency exchange risks reveals that the “Cheapest” way to exchange money is often the most dangerous.

-

Direct Costs (The Spread): The difference between the “Interbank Rate” (the rate banks use with each other) and the “Retail Rate” offered to the client. Luxury planners should aim for a spread of less than 1%.

-

Transfer Fees: Wire fees and intermediary bank charges. In 2026, many “Neobanks” offer zero-fee transfers, but their “Spreads” are often wider to compensate.

-

The Reliability Premium: Paying a slightly higher spread to a “Regulated FX Broker” who provides a dedicated account manager and “Proactive Market Monitoring.” This is effectively “Outsourced Intelligence.”

| Transfer Amount (USD) | Typical Retail Bank Spread | Specialist Broker Spread | Potential Annual Saving |

| $50,000 | 3.5% ($1,750) | 0.8% ($400) | $1,350 |

| $250,000 | 2.5% ($6,250) | 0.5% ($1,250) | $5,000 |

| $1,000,000 | 1.5% ($15,000) | 0.3% ($3,000) | $12,000 |

Tools, Strategies, and Technical Support Systems

-

Multi-Currency Accounts (MCA): Digital wallets (e.g., Airwallex, Revolut Business) that allow you to hold 30+ currencies simultaneously, avoiding unnecessary conversions.

-

Market “Stop-Loss” Orders: Automated instructions to buy currency if the rate drops below a “Pain Threshold,” preventing a catastrophic budget blowout.

-

Forward Contract “Drawdowns”: A flexible version of a Forward where you can take “Slices” of the locked-in currency as needed for deposit payments.

-

API-Integrated Accounting: Software that automatically pulls live FX rates into your budget spreadsheet to provide a “Real-Time” view of cost.

-

Volatility Calculators: Tools that simulate “Stress Tests”—showing how the budget looks if the currency moves +/- 5%, 10%, or 15%.

-

Direct GDS (Global Distribution System) Booking: For travel, booking in local currency through a GDS can sometimes bypass the “Currency Buffer” that hotels add to their USD-quoted rates.

-

Institutional FX Research: Access to “Daily Market Briefs” from major banks (Goldman Sachs, J.P. Morgan) to understand the “Macro Narrative.”

-

Credit Card “Foreign Transaction Fee” Audits: Ensuring all team members use cards with 0% FX fees, which can otherwise add an invisible 3% to every “On-the-Ground” expense.

Risk Landscape: The Taxonomy of Compounding Failures

Currency risk is rarely a “Linear” problem; it compounds with other logistical failures.

-

The “Liquidity Trap”: When a stakeholder hedges too much currency in a Forward Contract, and the project is canceled. They are still legally obligated to buy the foreign currency, often at a loss if the market has moved against them.

-

Counterparty Risk: The risk that the FX broker or bank itself becomes insolvent. In 2026, it is essential to ensure that your broker holds “Segregated Client Accounts” and is regulated by the FCA, FINRA, or local equivalent.

-

Settlement Risk (Herstatt Risk): The “Time Zone” gap where you have sent your USD, but the foreign currency hasn’t yet arrived in the vendor’s account due to bank holidays in the destination country.

Governance, Maintenance, and Long-Term Adaptation

To manage currency risks over a multi-year project, a “Governance Cycle” is required.

-

The “Inception Audit”: Identifying which expenses are “Local” (labor, venue) and which are “Global” (imported wine, celebrity talent paid in USD).

-

The “Monthly Re-valuation”: On the 1st of every month, update the budget with the current “Spot Rate” and adjust the “Contingency Fund” accordingly.

-

The “Trigger Point” Review: Setting specific dates (e.g., 90 days before the event) where a mandatory “Final Hedge” must be executed for all remaining balances.

Measurement, Tracking, and Evaluation

How do you evaluate if you have managed currency risk successfully?

-

Leading Indicator: “Percentage Hedged.” The ratio of committed future payments that are covered by a Forward or Option contract.

-

Lagging Indicator: “Variance to Original Baseline.” Did the final cost in the functional currency stay within 2% of the initial quote?

-

Qualitative Signal: “Peace of Mind Index.” Does the project manager spend more than 10 minutes a day checking exchange rates? If so, the hedging strategy is insufficient.

Common Misconceptions and Industry Myths

-

“Wait for the rate to get better”: This is gambling, not management. Market timing is notoriously difficult, even for professional traders.

-

“My bank gives me the best rate”: High-street banks are often the most expensive channel for FX, relying on customer “Inertia” to charge wider spreads.

-

“The USD is the strongest currency, so I’m safe.”Strength is relative. A “Strong USD” can still weaken against a specific regional currency due to localized interest rate hikes.

-

“Hedging is only for big amounts”: A 10% move on a $20,000 florist bill is $2,000—significant enough to impact the quality of other decor.

-

“Traveler’s checks or cash are best”: Physical currency carries “Theft Risk” and “Physical Conversion Costs” that are far higher than digital transfers.

-

“Cryptocurrency is a good hedge: Currently, the volatility of Crypto is significantly higher than that of G10 fiat currencies, making it a “Risk Multiplier” rather than a hedge.

-

“Forward contracts require 100% cash upfront”: Most brokers only require a 5-10% “Margin Deposit” to secure a Forward.

-

“Rates are the same everywhere”: There is no “One” exchange rate. The rate you see on Google is the “Mid-Market” rate, which is not available to retail or business customers.

Ethical and Practical Considerations

In the context of how to manage currency exchange risks, there is an ethical dimension to “Denominating Contracts.” Shifting all currency risk onto a small, local vendor in a developing nation by forcing them to accept a volatile local currency (while you pay in USD) can lead to “Vendor Insolvency.” A more sustainable, ethical approach is to share the risk or use a “Currency Collar”—where the price stays fixed unless the exchange rate moves by more than a pre-agreed percentage (e.g., 5%).

Conclusion: The Synthesis of Vigilance and Fiscal Engineering

The ability to how to manage currency exchange risks is a hallmark of sophisticated global stewardship. It represents a transition from a reactive “Consumer” mindset to a proactive “Managerial” posture. By acknowledging the inherent volatility of the floating exchange rate system and utilizing the conceptual frameworks of transaction and economic exposure, one can insulate a project from the vagaries of the market. The ultimate goal is not to “beat the market,” but to render the market irrelevant to the success of the mission. In an era of global interconnection, the most valuable currency is “Predictability.”